QUANT RESEARCH DECODED

Pulling back the curtain on Quantitative Finance Models

WHAT WE OFFER

From battle-tested trading indicators to personalized strategy sessions, we provide the tools and guidance you need to navigate quantitative finance with confidence.

The Armory

Access our collection of mathematically-driven trading indicators, each built on rigorous foundations from stochastic calculus, differential geometry, and advanced statistical methods. See Armory tab to integrate these powerful tools directly into your trading workflow. Due to platform limitations, these indicators are streamlined interpretations of our underlying models, intended for analytical insight rather than direct signal replication.

1-on-1 Sessions

Book a private consultation to dive deep into strategy development, indicator customization, or quantitative finance concepts. Whether you're looking to understand the math behind the models or need help implementing a custom solution, these sessions are tailored to your needs.

Reading List

Curated papers from various mathematical and statistical fields that form the theoretical backbone of our quantitative models. Start here to understand the mathematics.

THE ARMORY

Trading indicators powered by advanced mathematics and statistical modeling. Due to platform limitations, these indicators are streamlined interpretations of our underlying models, intended for analytical insight rather than direct signal replication.

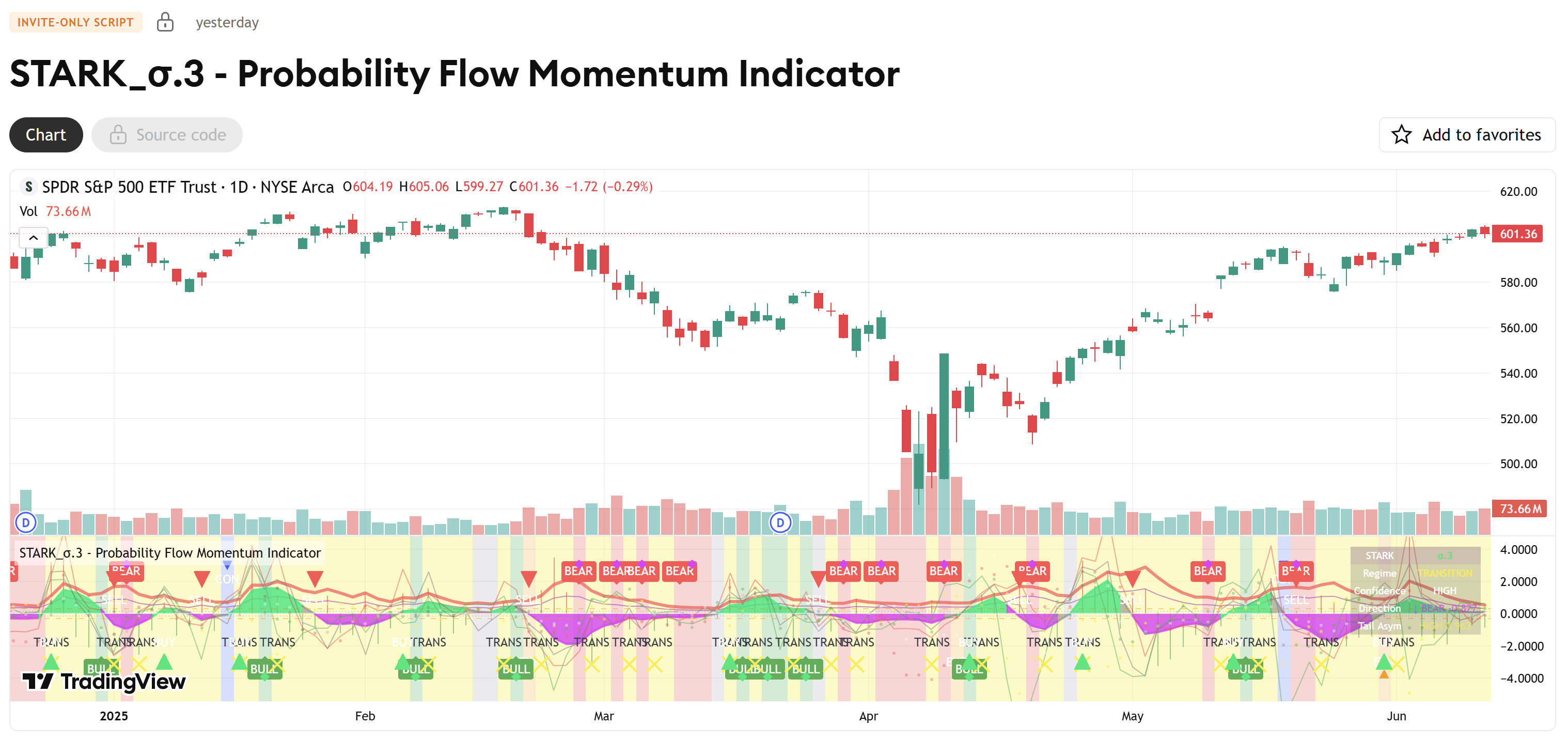

STARK σ.3

Probability Flow Momentum Indicator. Tracks how the "shape" of recent returns is shifting over time using optimal transport theory.

WAVE σ.9

Nonlinear Regime Classifier. Uses kernel methods to embed market states into feature spaces where complex patterns become detectable.

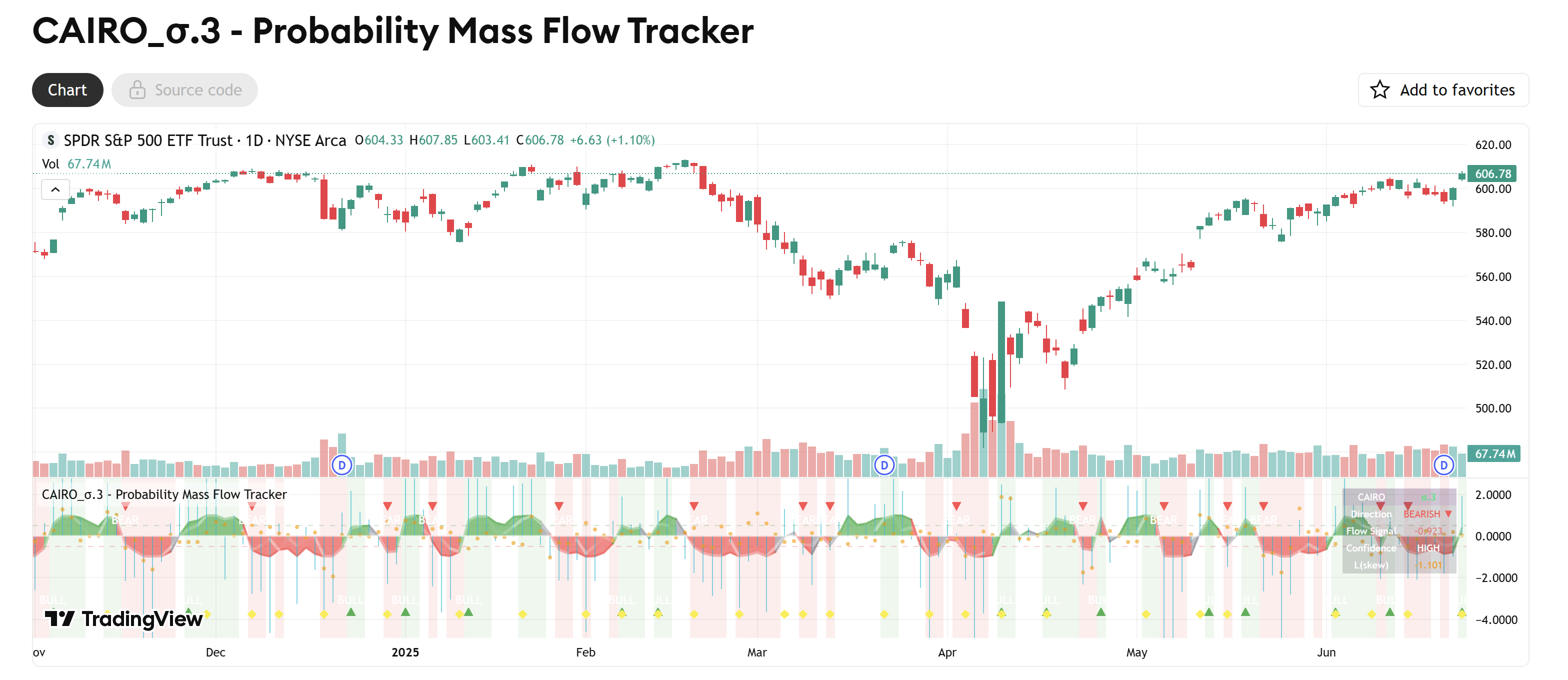

CAIRO σ.3

Probability Mass Flow Tracker. Analyzes how distributional moments evolve to capture the direction of probability mass movement.

ORBIT σ.1

Multi-Path Probability Oscillator. Evaluates competing trajectory scenarios simultaneously to detect structural alignment and regime transitions through interference pattern analysis.

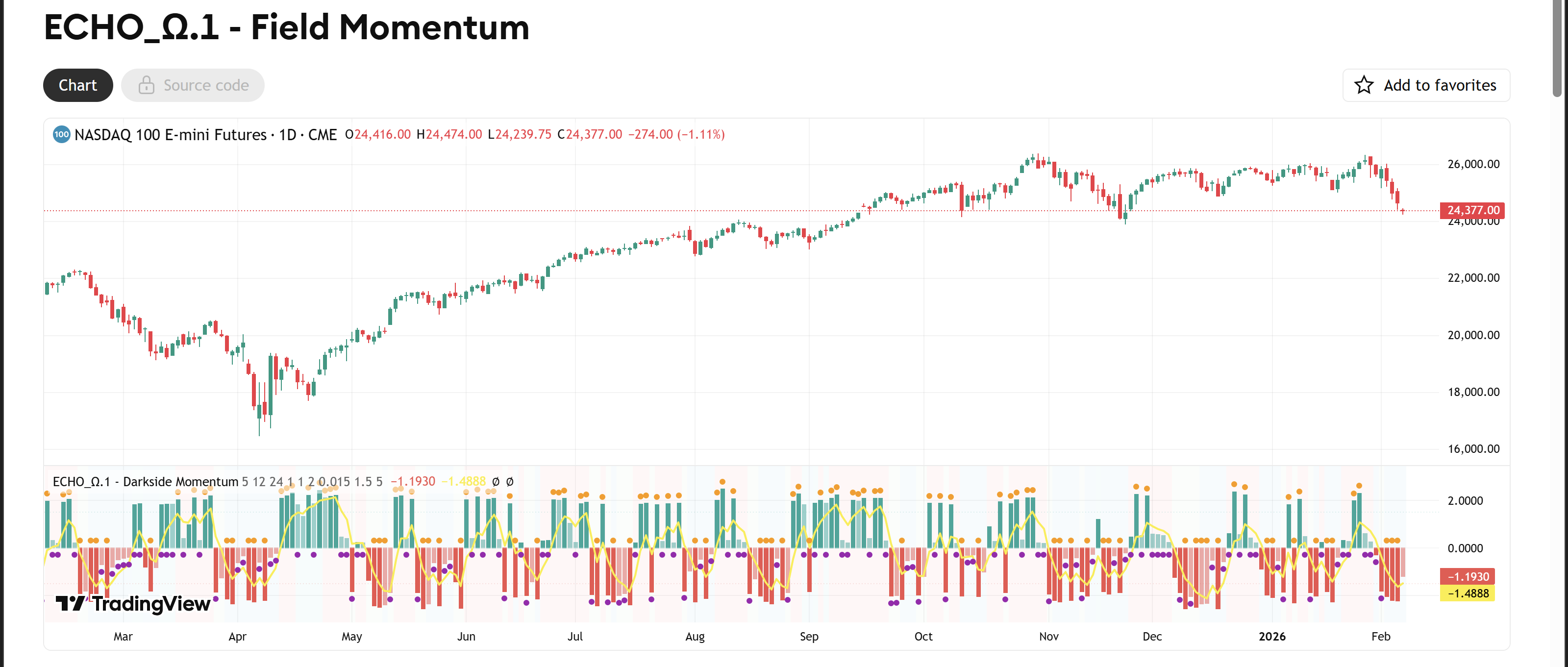

ECHO Ω.1

Field Momentum Indicator. Decomposes market dynamics into dual-coordinate energy states to detect momentum injection and exhaustion events ahead of traditional oscillators.

FLUX τ.3

Quantile Flow Field. Tracks how the shape of recent returns migrates across structural layers to reveal directional conviction before price confirms.

COMING SOON

Advanced volatility intelligence incoming. Shock & Regime Models designed to model explosive market moves. Stay tuned.

STARK σ.3

Probability Flow Momentum Indicator

STARK analyzes how market behavior evolves by observing changes in the shape and movement of outcomes. It measures the statistical momentum of probability mass flow to reveal regime shifts before traditional indicators.

Test the STARK_σ.3 indicator directly on TradingView. Add to your charts, customize parameters, and integrate with your trading workflow.

WAVE σ.9

Nonlinear Regime Classifier

WAVE applies advanced mathematical techniques to recognize when current market behavior matches historical bull, bear, or novel patterns. By analyzing the entire shape and structure of price action evolution, it identifies regime transitions before traditional indicators.

Test the WAVE_σ.9 indicator directly on TradingView. Add to your charts, customize parameters, and integrate with your trading workflow.

CAIRO σ.3

Probability Mass Flow Tracker

CAIRO analyzes higher-order distributional dynamics by computing derivatives of statistical moment evolution. It extracts directional flow signatures from asymmetry tracking to reveal momentum accumulation in market structure before price action confirms the move.

Test the CAIRO_σ.3 indicator directly on TradingView. Add to your charts, customize parameters, and integrate with your trading workflow.

ORBIT σ.1

Multi-Path Probability Oscillator

ORBIT evaluates multiple probabilistic pathways to form consensus market-direction forecasts. It analyzes algebraic structure across competing regimes, isolating high-conviction regime shifts ahead of traditional momentum signals.

Test the ORBIT_σ.1 indicator directly on TradingView. Add to your charts, customize parameters, and integrate with your trading workflow.

ECHO Ω.1

Field Momentum Indicator

ECHO models market dynamics as an evolving volatility system. It decomposes price action into dual-state coordinates and tracks the system's total balance to isolate moments where external forces inject momentum or where internal dissipation signals exhaustion, capturing regime structure that traditional oscillators miss entirely.

Test the ECHO_Ω.1 indicator directly on TradingView. Add to your charts, customize parameters, and integrate with your trading workflow.

FLUX τ.3

Quantile Flow Field

FLUX monitors the internal structure of market returns as a dynamic system that evolves over time. It measures how different layers of the return profile are migrating and whether they agree on direction. When all layers align, the move carries deep structural conviction. When they conflict, the apparent signal lacks foundation..

Test the FLUX_τ.3 indicator directly on TradingView. Add to your charts, customize parameters, and integrate with your trading workflow.

1-ON-1

SESSIONS

Deep-dive consultations tailored to your quantitative trading journey.

READING LIST

Foundational and frontier research behind quantitative finance. The mathematics underpinning our indicators and models.

A Primer on the Signature Method in Machine Learning

Path signatures as universal nonlinear features for sequential data, bridging rough path theory with practical applications in time series and financial data analysis.

Time Series Momentum

AQR's foundational study documenting significant time series momentum across asset classes — the backbone of what helicity is doing. Establishes that past returns predict future returns at intermediate horizons.

Dynamics of Implied Volatility Surfaces

Empirical study of the joint dynamics of implied volatility surfaces, revealing how surface evolution carries memory and structural persistence — directly applicable to regime-aware volatility modeling.

Waves and Mean Flows (2nd Edition)

Comprehensive mathematical treatment of wave–mean-flow interaction in geophysical fluid dynamics. Develops the Generalized Lagrangian Mean (GLM) framework, Eliassen–Palm flux theory, and nonlinear wave momentum transport. Establishes the theoretical foundations for how waves systematically reshape background flows in atmospheric and oceanic systems.

Price Dynamics in a Markovian Limit Order Market

Stochastic model of limit order book dynamics treating the order book as a continuous-time Markov process. Derives analytical results for price diffusion, spread dynamics, and the emergence of price discreteness from order flow mechanics.

Limit Order Books

Comprehensive review treating the order book as a discrete queuing system. Covers the statistical mechanics of how orders stack, deplete, and regenerate at price levels.

The Price Impact of Order Book Events

Empirical study of how order flow events propagate through the book. Shows how imbalances at one level predict price movement and quantifies the informational content of order book state changes.

Network Momentum across Asset Classes

Explores interconnections of momentum features across 64 futures contracts spanning commodities, equities, bonds, and currencies. Uses graph learning to reveal momentum spillover networks and construct cross-asset trading signals.

Follow the Leader: Enhancing Systematic Trend-Following Using Network Momentum

Combines univariate trend indicators with cross-sectional signals that capture momentum spillover from lead-lag relationships between markets. Demonstrates statistically significant improvements in Sharpe ratio and downside performance.

Volatility Spillovers in High-Dimensional Financial Systems

Identifies sparse volatility transmission networks across asset classes using regularized estimation. Separates own-volatility dynamics from cross-market spillover pathways to map how shocks propagate through financial systems.

See the Math in Action

These papers power our trading indicators. Explore the Armory to see theory become application.

Go Deeper

Want a guided walkthrough of these concepts and how they map to live markets? Book a 1-on-1.